Insurance Company Owned Life Insurance (ICOLI) is a tax and capital efficient investment strategy used by insurance companies to offset employee benefit costs. The insurance company is the owner and beneficiary of the insurance policies, and a select group of senior executives are the insureds. The cash value growth inside the policy is tax-deferred (tax-free if held until death) and death benefits are tax-free. However, what makes ICOLI such an attractive investment strategy is its favorable Risk-Based Capital (RBC) treatment.

The NAIC nor the rating agencies require a look-through to the underlying investment portfolio and instead base the counterparty risk on the issuing life insurance carrier. Most ICOLI sold today utilizes Private Placement Variable Universal Life (PPVUL) insurance, and these products typically offer hundreds of fund options including registered funds, low-cost index funds, and alternative funds. This allows an insurance company exposure to investments such as equities, high yield debt, private equity, private credit, and other Schedule BA assets without the substantial RBC charges. Removing, or mitigating, the capital reserve requirement, along with the tax benefits ICOLI offers, creates significant economic advantages as illustrated in the study below.

Case Study – Hypothetical ICOLI Purchase – Capital Advantage

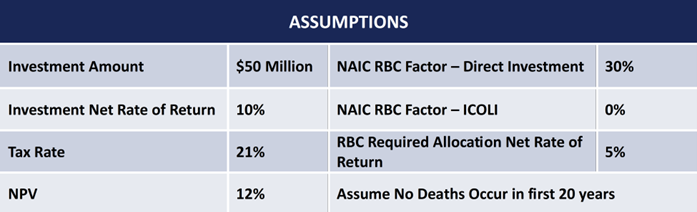

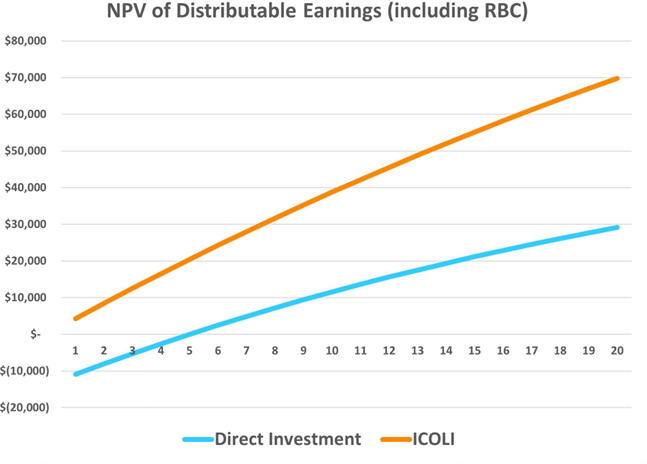

Scenario – a life insurance company purchases $50 million of ICOLI and allocates the premium into funds that would typically have a 30% RBC charge if held in the taxable investment portfolio. The chart below compares the risk-adjusted returns of an investment being placed directly into its investment portfolio versus that same investment utilizing an ICOLI structure.

No consideration of RBC redundancy of RBC covariance. Assumes end of first year RBC required allocation = $16.2M

A direct investment of this type of asset into a company’s taxable portfolio requires a high capital reserve provision. While the investment might produce impressive returns, the reality is that those returns must support an additional capital allocation. While the required allocation will also produce returns, these will likely be at a much lower level assuming investment in investment-grade bonds or the insurance company’s general account. This additional capital requirement really acts as an anchor and discourages many companies from allocating into certain asset classes with high RBC charges. ICOLI removes, or moderates, this capital drag and allows insurance companies to enjoy exposure to multiple asset classes, resulting in higher returns and enhanced overall investment diversification.

Why does ICOLI Receive Such Favorable RBC Treatment?

While it might seem too good to be true, there is a good reason for the differential treatment of ICOLI. When a company purchases ICOLI, it is presumably going to be owned until its maturity. The distribution at maturity is the death benefit, which includes the cash surrender value plus the net amount at risk. The cash surrender value includes the principal (or premium payment) plus all growth from the invested proceeds less insurance costs. The death benefit provides a layer of economic capital protection as the distribution amount at maturity will always be greater than the accumulated value of that investment. The regulators and ratings agencies view the life insurance company that issued the policy as the counterparty risk, not the underlying investments.

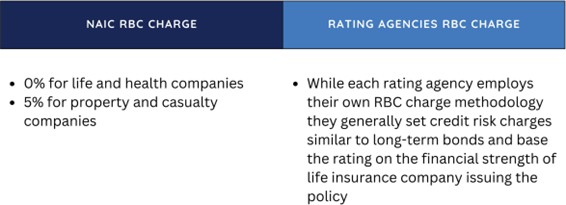

NAIC RBC Treatment

In 2018, the NAIC Statutory Accounting Principles (E) Working Group reviewed Private Placement Life Insurance (PPLI) to determine if it qualified as an admitted asset. The examination re-affirmed that PPLI, the most prevalent type of ICOLI, is an admitted asset. For NAIC/Regulatory purposes, ICOLI is considered an admitted ledger asset but not an invested asset and is categorized as an “other than invested asset”. Other than invested assets retain a 0% weight in the calculation of the asset risk component of the RBC requirement for life/health companies (C1/H1) and a 5% weight for P&C companies (R2).

Additional clarification and guidance can be found in Statement of Statutory Accounting Principles (SSAP) Number 21—Other Admitted Assets (paragraph 6). This states that ICOLI must qualify as life insurance under Internal Revenue Code (IRC) §7702 and must informally fund employee benefit plan(s). Also introduced were annual statutory statement requirements to report the cash value of the ICOLI as well as the allocation of the underlying investments in broad asset categories on line 21 (Other Items/Disclosures) in the “Notes to Financials” section.

Rating Agency RBC Treatment

Rating agencies use the same risk-based capital treatment they apply for long-term bonds to ICOLI with the charge based on the rating of the insurer. In November of 2023, S&P Global Ratings’ Review published their updated Insurer Risk-Based Capital Adequacy Methodology and Assumptions. In it they reexamined how they assessed ICOLI, concluding:

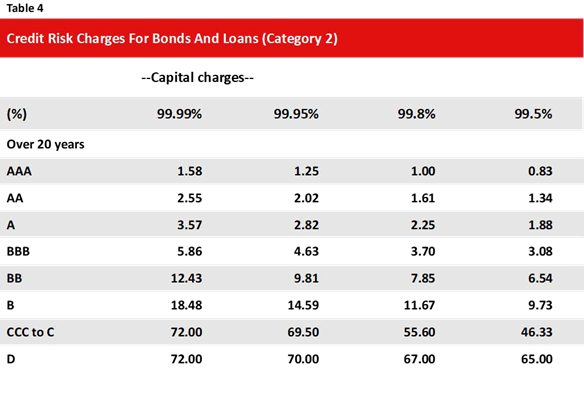

- Credit risk charges associated with bonds and loans are applied to COLI assets. The charge is based on the rating on the insurance counterparty and assume the tenor is over 20 years (see Table 4).

- Assumes that the insurer has the willingness and ability to hold the COLI asset until maturity and that volatility in the carrying value of the COLI asset does not represent a material risk.

Table 4 Source: “Criteria | Insurance | General: Insurer Risk based capital Adequacy – Methodology and Assumptions” – S&P Global Ratings

This updated methodology and assumptions for analyzing RBC adequacy by S&P reflected a more considerate and accurate analysis of ICOLI from their prior model. The previous model included the RBC charge within all miscellaneous write-in assets and carried a higher charge ranging from 5.0%-8.1%. Under the new methodology, using Table 4, purchasing ICOLI from an insurer with ratings from A to AAA can now expect a lower charge range of 0.83%-3.57%.

Use of ICOLI is Growing

ICOLI is not a new concept in the insurance industry but, until recently, the adoption of this strategy has been prolonged. This may be due to the regulatory ambiguity prior to the recent guidance mentioned above. Insurance companies have utilized Corporate Owned Life Insurance (COLI) for decades to informally fund traditional non-qualified deferred compensation plans. However, it wasn’t until recently that companies started applying ICOLI as a strategic treasury asset to offset aggregate employee benefit costs.

The 2018 NAIC Statutory Accounting Principles (E) Working Group put ICOLI under a microscope and reaffirmed ICOLI’s status as an admitted asset and kept its qualification as an “other than invested asset” along with the associated favorable RBC treatment. This proved to be the regulatory North Star insurers were looking for to gain comfort investing in ICOLI and seems to be the catalyst for subsequent progress.

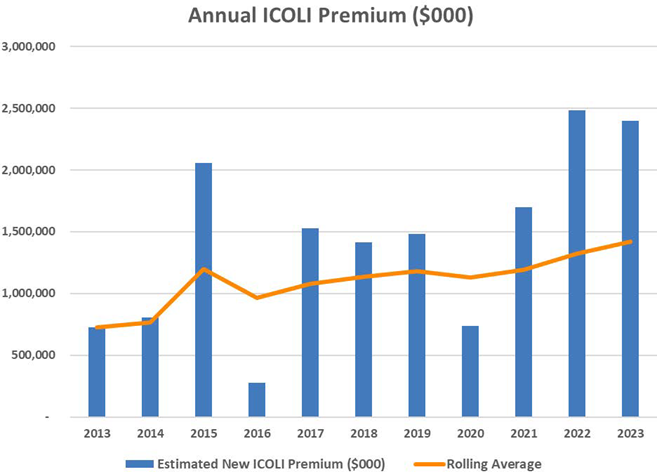

The chart below illustrates recent strong ICOLI sales growth. The average annual premium from the years 2019-2023 (removing 2020 due to COVID) is over $2 billion and the average annual premium from 2021-2023 is $2.2 billion with the total 2024 premium projected to exceed $2.5 billion.

Data source: S&P Global Market Intelligence; NAIC Annual Statements

Note also the large premium in the year 2015. This was due almost entirely from a single purchase. This acquisition was significant not only due to its size but because it pioneered the use of customized private market underlying funds which helped highlight the favorable capital treatment ICOLI provided as well as the possibility to access a wide variety of asset classes.

The evolution of ICOLI is not only evident by the premium growth but also by the growth of the creative and diversified investment options offered. In addition to the hundreds of registered funds, low-cost index funds, and various alternative funds available, insurers may be able to access closed private equity and private credit funds within the ICOLI infrastructure as well as the opportunity for custom portfolios.

ICOLI Provides a Unique Opportunity

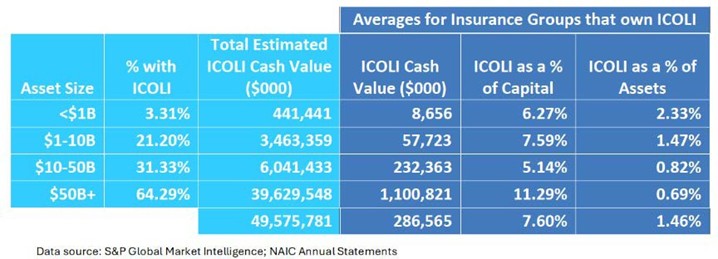

ICOLI has become a well-established asset with an estimated 64% of insurance groups over $50 billion in assets, and almost a third of the groups between $10-50 billion in assets, owning ICOLI (see chart below).

Due to the recent regulatory clarity and significant recent ownership by larger insurance companies, this has established an increased comfort level and growing interest for companies in the mid-size and smaller market to investigate an ICOLI purchase.

Is ICOLI too good to be true? While due diligence must be done by any company to determine if ICOLI is appropriate, the fact is there are limited investments available to insurance companies to optimize their risk/return profile while improving their earnings, surplus, and financial strength. ICOLI is one of the few options an insurance company can choose to potentially enhance its tax-adjusted earnings, gain favorable risk-based capital (RBC), and expand investment choices. Most insurance companies owe it to themselves to explore how they might potentially benefit from implementing an ICOLI program.